Introduction

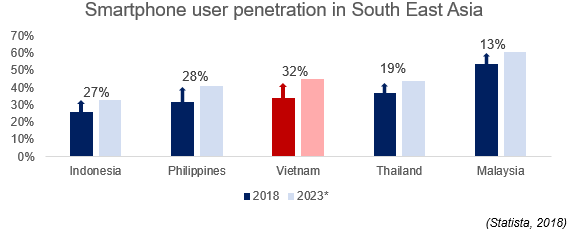

Vietnam has been through a spectacular digitalization during the last few years. From 2017 to 2019, internet penetration increased from 53% to 66% and the share of active social media users has gone from 48% to 64% in the same period. (Kemp, 2017 and 2019) As of 2018, 32% of the population owns a smartphone.

Despite these figures, the popularity of mobile point-of-sales (mPOS) solutions – paying with your smartphones in shops – has not caught up to that of its Asian peers. Today however, a number of factors in Vietnam are giving room for mPOS payments to grow as it has done in neighboring countries. In combination with certain demographical trends, mPOS may finally present itself as a viable substitute to cash in the future for Vietnam.

What are mPOS payment solutions?

MPOS payments is an increasingly popular form of digital payment around the world, which has emerged with the rise of smartphones. For the consumer, it simply involves downloading an application, in which there is a QR-code scanner or similar function that is linked to the user’s bank account. Registered brick-and-mortar store owners own the solution’s terminal, which the consumer then can scan to complete a purchase (Thao, 2018). The applications are often in the form of e-wallets where mPOS is one feature. Depending on the providers’ services, e-wallets enables users to pay for everything from electricity, water, and TV, to offer other integrated services such as sales of flight and movie tickets.

Considering mPOS is a direct competitor with debit and credit cards, domestic banks such as Vietinbank and Sacombank have entered the market and let customers take up loans and administer their insurance policies directly in the app. Generally, there has been a burst of investments in the market recently, which has created a myriad of differentiated contenders. Most of these have been small fintech companies funded with venture capital. Some noteworthy domestic players in the Vietnamese e-wallet and mPOS industry include:

- MoMo, founded 2014, backed by Standard Chartered Bank and Goldman Sachs (The Asian Banker, 2018)

- Zalo Pay, founded 2016, backed by VNG Corporation

- 123pay, founded in 2016, backed by VNG Corporation

- National Payment Corporation of Vietnam (NAPAS), founded in 2004, backed by the State Bank of Vietnam

- vn, founded in 2013, backed by Sacombank, Vietinbank, Mandiri, Bluebird, SyberSource

- OnOnpay, founded 2015, backed by Fenox Venture Capital, Captii Venture, Gobi Partners

Foreign entrants include:

- iBox, from Russia, entered Vietnam in 2014, backed by InVenture Partners, Almaz Capital, ENS Group

- SoftPay Mobile, from Singapore and present operations in SEA, backed by Life.SREDA

- WeChat, for Chinese tourists in cooperation with VIMO from 2017 (Ly, 2017)

- Alipay, for Chinese tourists in cooperation with NAPAS from 2017 (Ly, 2017)

Vietnam’s surprisingly low Mobile POS Payments and preference for cash

The Asia Pacific region has generally been early adopters of mPOS payments, and its usage is significantly higher than in the West despite lower internet penetration. In monetary value, e-wallet purchases accounted for 27% of point-of-sales transactions in Asian Pacific countries, compared to only 3% in North America during 2017. Generally, the Asia Pacific region has a preference for mPOS and cash, while North America has a preference for debit and credit cards. Vietnam, however, is an almost completely cash-based society with a staggering 86% of transaction value from cash payments and only 2% from e-wallets during 2017 (Worldpay, 2018).

What has caused Vietnam to differ so dramatically from its fellow Asian countries, and even the West? It is not the level of mPOS user penetration. In fact, Vietnam’s share of mPOS users in terms of population was almost 50% higher than in North America in 2017 – 8.9% versus 6.2% (Statista, 2019). Compared to Asia Pacific, Vietnam’s user penetration was about half – 8.9% versus 17.9%. This may partially explain the lower mPOS transaction value in Vietnam, but the fact that e-wallet (mPOS) payments accounted for a mere 2% of total POS purchase value in Vietnam, which is only 1/15th than that of Asia Pacific’s 27%, indicates that there must be other reasons behind the situation.

Other factors are in play, of which a historically rooted skepticism toward retail banking amongst Vietnamese people is the most evident one. Earlier, high inflation rates and low interest rates offered to consumers have not incentivized people to open bank saving accounts (Larimer, 1994). Instead, people have relied on informal banking networks within their social networks, usually in their home village, known as “phuongs”. The phuongs function by pooling inhabitants’ money and holding sporadic tea meetings in order to collectively decide interest rates and loan terms (Stocking, 2007). Besides from being more personal, these networks have offered interest rates that have been superior to those of commercial banks. By committing to funds given by family members, default rates have been minimal; inability or unwillingness to repay would make you ostracized from the village permanently.

How does this relate to the unpopularity of mPOS payments? E-wallets have traditionally had to be connected to a bank account to draw funds from when making transactions. Even today very few people in Vietnam have bank accounts registered to their name, part of the reason being the previously discussed family lending networks. Another dimension is the trustworthiness and touch-and-feel that only cash can provide. Suspicion against fraud and the historically limited accountability of legal institutions in Vietnam has led to a relationship-based business environment, in which people have preferred to conduct business with people they know, with payments they know; cash. Finally, the banking system is not integrated properly, which slows downs money transfers between consumers with different banks considerably.

A large informal economy, with double accounting (a common practice among companies where two books are established – one for the official tax records and one with the company’s true performance) being the norm, has emerged from this. Cash as a payment is a prerequisite for this behavior as it allows for transactions to go unrecorded and corporate income taxes to be avoided. For business owners, this also eases logistics in terms of documentation. In Vietnam, VAT is collected through so called “red invoices”, which are physical copies of paper that are required to be signed and kept by both parties for all transactions. In addition to this, physical papers with official stamps from the company are also necessary to be issued. Thus, the cost and inconvenience of formal transactions has resulted in the rise of an extensive informal economy. In terms of logistical ease, payments by card or mPOS are superior since they are digitally recorded, but are by consequence difficult to tamper with and thereby also subject to tax.

Things are changing – Mobile POS Payments are picking up speed

In order to attract customers, actors in e-commerce had to come up with a payment system that appealed to the strong preference for cash in Vietnam. This resulted in a payment method called Cash-on-Delivery (COD), in which the customer simply pays the delivery in cash when they receive their item. However, this option is becoming increasingly unfavorable to some businesses, as the logistics of cash handling in cross-border transactions in particular has been troublesome (EBI & Vietnam E-Commerce Association, 2019). Today e-commerce platforms are accepting COD payments more as a means to gain customers and create brand trust in preparation for a switch to electronic payments. Banks too, often having stakes in the industry by developing proprietary mPOS solutions, have actively been trying to discourage cash payments in favor of digital payments. A number of banks are attempting to circumvent the entire problem of dealing with an unbanked population by letting people top up their e-wallets at convenience stores with cash. Some have been offering shoppers discounts up to 10% on goods in stores for using e-wallets and QR codes (Mai, 2019), whereas others have offered vouchers (one example being Samsung Pay that offered users daily vouchers of $1.31 during 2018 (VN Economic Times, 2018)). Although this encourages businesses to adopt mPOS, it still does not seem to outweigh the disadvantage of paying corporate income tax whenever purchases are conducted digitally and legally.

The infrastructure for e-wallet payments has not been optimal either. One issue has been the fragmentation of QR codes that originates from the disorganized mix of competitors in this immature market, which as a consequence has added additional complexity to the implementation of mPOS terminals for businesses. Currently the National Payment Corporation of Vietnam (NAPAS) is developing a common QR code (Mai, 2019) that can be used for all competing brands. Hopefully this could mitigate the fragmentation issue and encourage widespread adoption of mPOS solutions. Especially the smallest actors in the Vietnamese economy, such as street food vendors, would benefit from this. Of all businesses, micro-sized enterprises possess the lowest technological proficiency and least amount of resources. Thus, these are the businesses that are most prone to avoid mPOS if its installation becomes too complicated. Considering 74.4% of businesses were micro-sized enterprises in Vietnam in 2017 (General Statistics Office, 2018), it is an important and salient matter.

A digital transformation in point-of-sales payments is strongly supported by the Vietnamese government, both on local and national levels. The Vietnamese Government’s Decision No. 1563 was taken to adopt the E-Commerce Development Master Plan; a plan that seeks to enhance effectiveness within legal frameworks in digital marketplaces by creating a national E-Payment system applicable to all E-commerce by 2020. Regarding mPOS specifically, formulated goals include distributing mPOS terminals to all retail stores (e.g. department stores, supermarkets, and modern distribution centers) before the specified timeline (EU-Vietnam Business Network, 2018). More recently, Resolution 02/NQ-CP, which was released in early January 2019, details how The People’s Committees of municipalities and provinces must direct schools, hospitals, providers of water, electricity, telecommunications and more sectors to co-ordinate with banks and payment providers to facilitate cashless payments before the end of the year, with mPOS explicitly being the preferred means. In addition, commercial banks and payment intermediaries must construct QR code standards before the third quarter of 2019 (VietNamNews, 2019).

Finally, observable macro trends suggest Vietnam’s transition from all-cash to cashless is indeed possible. Although the majority, 64% in 2017 of the Vietnamese population (World Bank, 2018), is still living in rural areas, largely disconnected from the institutionalization the rest of the country is undergoing, urbanization is rapidly increasing. This will likely shift focus away from the informal “Phuong” banking networks that operate from people’s home villages, toward conventional retail banking. In addition, digitalization is still in process, allowing for a higher mPOS payment penetration during coming years. Lastly, young adults (<35 years) are more positive and trusting toward banks than elderly (Stocking, 2007) and account for a remarkable 60% of the population today (PwC & VCCI, 2017), which truly paves way for a mPOS breakthrough.

Conclusions

Undoubtedly, significant obstacles are still in the way for a complete transition. A major challenge is to reach the two thirds of the Vietnamese population that still live in rural areas and lack any connection to the modern lifestyles of their urban peers. The historical distrust toward the legal system and banking sector will remain, as well as the financial benefits of keeping transactions in cash for the purpose of tax-avoidance.

Despite Vietnam’s lag behind other countries in terms of mPOS development, the future is looking more promising. The fragmented digital infrastructure is being reconstructed, and strong-willed actions to replace cash with mPOS payments are taken by both the Government and commercial banks. Long-term macro trends are in favor of mPOS too; a large young population that is extensively digitalized is moving from the countryside to the cities. Their positive attitude toward mPOS payments and willingness to modernize supports a strong market outlook. All in all, the perceived growth potential has been identified by investors, indicated by new entrants appearing continuously. The environment for mPOS payments is certainly a highly dynamic one with many opportunities for improvement and angles of entry.

References

EBI & Vietnam E-Commerce Association. (2019). Vietnam E-Business Index 2019. Hanoi: Vietnam E-Commerce Association.

EU-Vietnam Business Network. (2018). E-Commerce Industry in Vietnam Edition 2018. Ho Chi Minh City: EU-Vietnam Business Network.

General Statistics Office. (2018). Results of the 2017 Economic Census. Hanoi: Statistical Publishing House.

Kemp, S. (2017 and 2019). DIGITAL IN 2018 IN VIETNAM. New York, New York, USA: wearesocial; Hootsuite. Collected from sdf

Larimer, T. (29 December 1994). Vietnamese Still Bank The Old-Fashioned Way. Collected from The Washington Post: https://www.washingtonpost.com/archive/politics/1994/12/29/vietnamese-still-bank-the-old-fashioned-way/f0601e71-a4db-4aae-ac47-9466db6f2ad9/?utm_term=.2a482330d84f den 02 July 2019

Ly, V. (15 November 2017). WeChat Pay e-wallet launched in Vietnam . Collected from The Saigon Times: https://english.thesaigontimes.vn/57052/wechat-pay-e-wallet-launched-in-vietnam.html) 3 July 2019

Mai, N. (23 February 2019). Non-cash payments finally becoming more popular in Vietnam. Collected from Vietnamnet: https://english.vietnamnet.vn/fms/business/218017/non-cash-payments-finally-becoming-more-popular-in-vietnam.html) 2 July 2019

PwC & VCCI. (2017). Spotlight on Viet Nam: The leading emerging market. Economic report, Ho Chi Minh City.

Statista. (2018). Smartphone penetration in South East Asia. Collected from Statista: https://www.statista.com June 2019

Statista. (May 2019). Mobile POS Payments. Collected from Statista: https://www-statista-com.ez.hhs.se/outlook/331/102/mobile-pos-payments/europe#market-revenue 02 July 2019

Stocking, B. (14 November 2007). Foreign banks encounter cultural barrier in Vietnam. Collected from The New York Times: https://www.nytimes.com/2007/12/14/business/worldbusiness/14iht-dong.1.8746227.html 2 July 2019

Thao, N. (2 July 2018). Vietnam Economic Views – Ministry of Industry and Trade. Collected from http://ven.vn/e-wallet-services-in-fierce-competition-for-vietnamese-consumers-33346.html 02 July 2019

The Asian Banker. (12 September 2018). How a fintech outgrew banks in the mobile wallet market in Vietnam . Collected from The Asian Banker: http://www.theasianbanker.com/updates-and-articles/how-fintech-outgrew-banks-in-the-mobile-wallet-market-in-vietnam 3 July 2019

VietNamNews. (3 January 2019). Government intensifies support for non-cash payment methods. Collected from VietNamNews: https://vietnamnews.vn/economy/483138/government-intensifies-support-for-non-cash-payment-methods.html#z79CL1Q77YP6Klp3.97 2 July 2019

VN Economic Times. (14 January 2018). Way to pay. Collected from Vietnamnet: https://english.vietnamnet.vn/fms/business/193493/way-to-pay.html) 2 July 2019

World Bank. (2018). Rural population (% of total population). Collected from World Bank: https://data.worldbank.org/indicator/SP.RUR.TOTL.ZS?locations=VN 2 July 2019

Worldpay. (2018). Global Payments Report November 2018. New York City: Worldpay.