Vietnam has over the last decade developed into one of the world’s most dynamic markets with increasing domestic purchasing power and a young market, so there is still plenty of opportunity in the market. Here we try to provide a short overview of the M&A landscape in Vietnam, specifically towards Small and Medium sized companies (SMEs).

1. Small and medium-sized enterprise (SME) in Vietnam

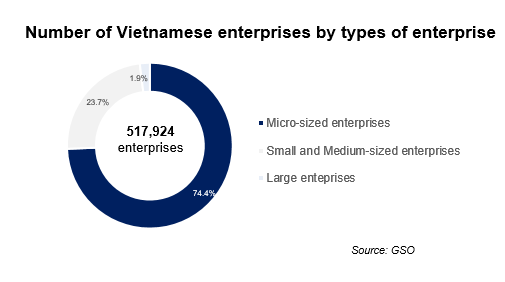

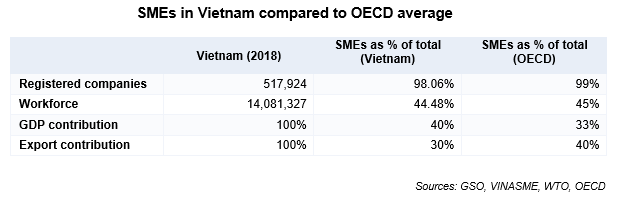

According to results of Economic Census in 2017 by General Statistics Office of Vietnam (GSO), around 98% of all companies in Vietnam are classified as a SME*. Of SMEs around 75% are considered as micro-enterprises (such as small restaurants and small agricultural businesses) with a total market size of 97 BUSD, it is a major part of the Vietnamese economy, however the net result of these companies records a negative of 1.2 BUSD in profits.

The low profitability of micro-enterprises is due to operational inefficiencies and lack of strategic direction. These companies also have difficulties attracting capital as a lack of organization and professionalism make them a high-risk investment with small potential for scalability.

For other SMEs, the issue of accessing to capital is still there, despite many companies recognizing the increasingly competitive landscape, their lack of financing limits competitiveness and growth. More and more SMEs are taking new strategic routes such as integrating digital tools and new technology to existing operations, concentrating on niche market, cooperation with other SMEs or larger enterprises, etc.

The opportunity exists both for local enterprises and foreign investors looking for acquisition targets and long-term partners to engage in M&A processes for future success.

2. Statistics about M&A deals

General overview

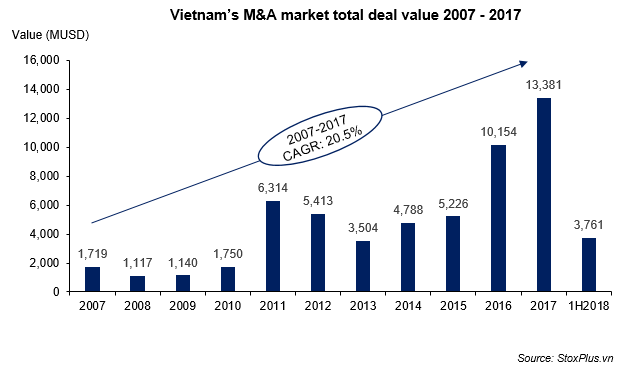

Total value of M&A deals in Vietnam in 2017 reached the record of 13.4 BUSD (+31.8%), with a CAGR of 20.5% in the period 2007 – 2017. This outstanding result was fueled by mega deals in F&B and real estate industry such as the acquisition of SABECO by ThaiBev, Vinamilk by Jardin C&C or the IPO of Vincom Retail.

Market sizes and deals

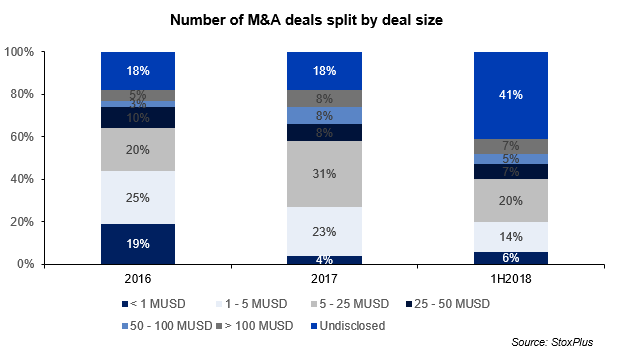

Around 70% of M&A deals in Vietnam happened in the SMEs space with deal values ranging between 1 – 25 MUSD. The number of large M&A deals was increasing due to the privatization of large SOEs and more consideration in M&A as an exit or development strategy, but in the next few years, SMEs are forecasted to continue making up the majority of the deals.

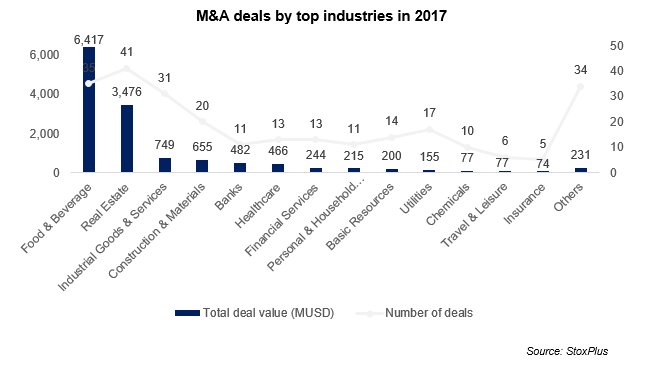

Industries

The two largest industries for M&A in Vietnam are Food & Beverage and Real Estate which in 2017 contributed more than 70% of the total deal value and close to 30% of the total deals made. The most noticeable deals in these industries were the acquisition of SABECO by ThaiBev at 4.7 BUSD and the 734 MUSD deal from Vincom Retail IPO. Other industries such as Industrial Goods & Services, Construction & Materials and Utilities were also active due to high market demand and strong performance along with stable macroeconomic conditions in Vietnam.

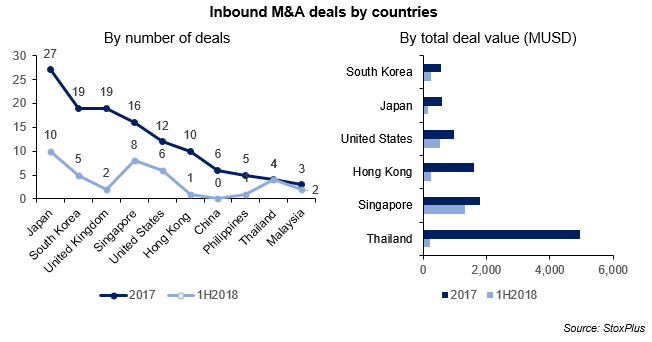

M&A deals by countries

In 2017, 44% of total transactions were conducted between Vietnamese enterprises, but the value just reached 1.6 BUSD (11.6% of the total value) as the majority of domestic deals are for SMEs. On the contrary, cross-border M&A almost always focused on bigger ticket sizes and contributed to 11.8 BUSD (87.9% of the total value). The most active investors come from Thailand, Singapore, China, South Korea, Japan and USA. While Japanese investors focused on aviation, petroleum and pharmaceuticals, Singaporean investors paid more attention to real estate projects. Thailand, as the most active investor, focused mainly on retail and construction materials.

3. Reasons for SMEs to participate in M&A transactions

As a transitioning economy, Vietnamese entrepreneurs and business owners view their companies as a way to make a living or to enable future generations to have a better starting point in life. As such, there is less consideration for exit strategy or plan to divest the company to external investors. Therefore, the common reason for domestic companies to engage in a deal process would be to promote further business expansion and competitiveness. This strategy can pursue along 2 paths – horizontal and vertical integration.

- For horizontal integration, companies acquire or merge with other players in the market to increase the capacity and market share by gaining competitiveness in price, market, technology, etc. against larger incumbents. For vertical integration, companies would look to integrate further up or down the value chain looking to either the supplier or distribution of their products/services. Combining these entities gives a higher control of each process from input, production and the final sales of the product/services as a “full-package” deal for customers.

Another common route for business owners is a complete divestment and is usually motivated by the current owner’s retirement or other personal issues, especially family-owned enterprises heavily depending on the founder for its future development or newly formed businesses whose founders have an already envisioned exit strategy from the inception.

4. Potential industries for SMEs to do M&A

Consumer goods and retail

Consumer goods and retail, especially for F&B products, have in the recent years been on the mind of both foreign and domestic players looking to leverage the increasing consumer purchasing power and to gain a strong position in the market. In the local market, we see a transition from small scale retail shops towards a more branded scene of bigger retail chains, coupled with the emerging e-commerce industry.

Despite a fierce competition for market share, this industry will continue to be on the top for investors looking towards Vietnam – niche areas of this industry will be the next move for investors as the general market multiples keep increasing.

Agriculture

Vietnamese agriculture is expected to receive a wave of new developments from applying technology to improving the value chain for processing and distribution. For the M&A space, SMEs are expected to either be outcompeted and acquired by larger players or merge to deliver higher value-added products and draw better use of their existing networks and capital.

Technology

Vietnam is considered as an attractive start-up hub for large IT corporation such as Intel, Google, Microsoft, etc. Along with a boost in innovation & technology start-ups, Vietnam welcomes increased attention from investors willing to take on higher risks in SMEs. There are four main sectors where the investment space is becoming increasingly crowded, namely E-commerce, Telecommunication, Fin-tech and Ed-tech. Furthermore, some active venture capitalist funds such as IDG Ventures, CyberAgent Ventures, etc. have invested in Vietnamese renowned IT startups including Vinagame, Topica EdTech Group, Luxstay, Leflair, etc.

Logistics

The logistics industry in Vietnam today is a fragmented market which is partly regulated by Foreign Ownership Limitations. According to Vietnam Logistics Association, over 1300 logistic companies are active in Vietnam today and are under big pressure from larger foreign players due to the fact that about 80% of all logistic companies in Vietnam are local but only contribute for 25% of the market share. Today the market makes up around 3% of GDP and the Vietnamese Government targets it to reach 10% of GDP by 2025. With increasing demand from customers that companies deliver a full logistic solution, the number of M&A transactions in coming years are expected to increase rapidly as other regional players are looking to expand their network throughout South-East Asia.

Successful transactions can provide large sources of capital, technology transfer, management capability to increase the competitiveness and market share of domestic companies.

5. Conclusions

Vietnam’s M&A market is expected to keep its fast pace in the coming years. The dominant sectors will remain in Consumer Goods, Retail and Real Estate with increased deal flow across areas in telecommunication, pharmaceutical, energy and education.

The coming years are expected to see some major deals as the privatization of State-owned Enterprises continues and the appetite from large foreign investors increases. However, it will be within the SME space where most value needs to be uncovered as they will continue to make up a big part of Vietnam’s economy and are present throughout all provinces of Vietnam.

In the next article about M&A in Vietnam, we will take a further look to the preparation and steps for domestic companies preparing for a deal process to increase valuation and reduce the risk.

TBRC is a trusted M&A advisor part of the network CDI Global, providing services for local and foreign entities looking to develop their M&A strategies. For more information about us and our services please visit our website here.

———————————————————————————————————

* According to General Statistics Office of Vietnam, in 2017, the total labor force in Vietnam is 54.8 million people. About 14 million people work in enterprises while 13 million people work in other economic establishments such as cooperatives, individual business establishments, administrative units, etc. The majority of labor force (about 27 million people) is self-employed such as farmers , fishermen, sellers in wet market, street vendors, motorbike taxi drivers, etc.